All Categories

Featured

Table of Contents

The are entire life insurance policy and global life insurance policy. The cash value is not added to the fatality benefit.

After ten years, the cash value has actually expanded to approximately $150,000. He gets a tax-free financing of $50,000 to begin a service with his sibling. The plan car loan rates of interest is 6%. He repays the funding over the next 5 years. Going this course, the rate of interest he pays goes back into his policy's money value rather than a banks.

Royal Bank Visa Infinite Avion Card

The idea of Infinite Banking was created by Nelson Nash in the 1980s. Nash was a money expert and follower of the Austrian college of business economics, which advocates that the worth of goods aren't explicitly the outcome of conventional financial frameworks like supply and need. Rather, individuals value money and goods in different ways based on their economic status and requirements.

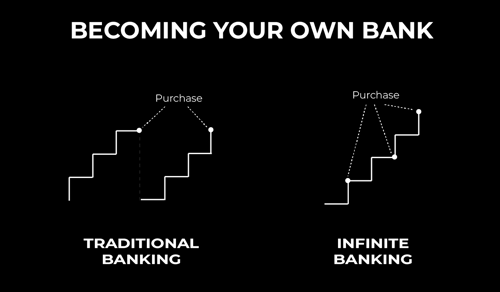

One of the pitfalls of standard banking, according to Nash, was high-interest rates on financings. As well several individuals, himself included, obtained into financial difficulty as a result of dependence on banking organizations. Long as banks established the passion prices and finance terms, people didn't have control over their very own wide range. Becoming your very own lender, Nash identified, would place you in control over your monetary future.

Infinite Financial requires you to possess your economic future. For ambitious individuals, it can be the best financial tool ever. Here are the advantages of Infinite Banking: Probably the single most helpful aspect of Infinite Banking is that it boosts your cash money flow.

Dividend-paying entire life insurance policy is really reduced danger and uses you, the insurance holder, a wonderful bargain of control. The control that Infinite Banking supplies can best be organized right into 2 groups: tax benefits and asset securities - infinite banking concept pros and cons. One of the reasons whole life insurance policy is ideal for Infinite Financial is how it's strained.

Infinite Banking Insurance Companies

When you utilize entire life insurance for Infinite Financial, you enter into an exclusive agreement in between you and your insurance policy firm. These protections may vary from state to state, they can include security from property searches and seizures, protection from reasonings and security from financial institutions.

Whole life insurance policy policies are non-correlated assets. This is why they work so well as the financial foundation of Infinite Banking. Despite what happens in the marketplace (stock, actual estate, or otherwise), your insurance coverage preserves its well worth. A lot of individuals are missing this essential volatility buffer that aids secure and grow riches, instead splitting their cash right into 2 pails: checking account and financial investments.

Whole life insurance coverage is that 3rd container. Not just is the rate of return on your entire life insurance coverage plan guaranteed, your death advantage and premiums are also assured.

Here are its primary advantages: Liquidity and availability: Plan fundings supply instant access to funds without the limitations of traditional financial institution financings. Tax performance: The money worth expands tax-deferred, and plan lendings are tax-free, making it a tax-efficient device for building riches.

Infinite Bank Glitch Borderlands 2

Property protection: In several states, the money value of life insurance policy is shielded from lenders, adding an additional layer of financial security. While Infinite Financial has its benefits, it isn't a one-size-fits-all service, and it comes with considerable drawbacks. Here's why it might not be the most effective strategy: Infinite Banking usually requires detailed policy structuring, which can confuse policyholders.

Think of never ever needing to fret about small business loan or high rates of interest once more. What if you could borrow cash on your terms and develop riches concurrently? That's the power of infinite banking life insurance policy. By leveraging the cash worth of entire life insurance policy IUL policies, you can expand your riches and borrow cash without depending on traditional banks.

There's no collection finance term, and you have the liberty to choose the repayment routine, which can be as leisurely as settling the funding at the time of fatality. This flexibility encompasses the servicing of the lendings, where you can choose interest-only repayments, maintaining the car loan balance flat and workable.

Holding money in an IUL dealt with account being credited passion can frequently be much better than holding the money on deposit at a bank.: You've always desired for opening your very own bakery. You can borrow from your IUL plan to cover the first costs of renting out a space, purchasing equipment, and hiring staff.

Wealth Nation Infinite Banking

Individual finances can be gotten from conventional financial institutions and lending institution. Right here are some bottom lines to consider. Charge card can offer an adaptable method to borrow cash for really short-term durations. However, obtaining cash on a charge card is typically very costly with annual percentage prices of interest (APR) frequently getting to 20% to 30% or even more a year.

The tax therapy of policy financings can differ substantially relying on your nation of residence and the specific regards to your IUL policy. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, plan car loans are generally tax-free, offering a substantial benefit. In various other jurisdictions, there may be tax ramifications to take into consideration, such as potential taxes on the funding.

Term life insurance policy only provides a death benefit, without any kind of cash worth buildup. This implies there's no money value to borrow versus.

However, for car loan officers, the substantial laws imposed by the CFPB can be viewed as cumbersome and limiting. First, finance police officers often suggest that the CFPB's guidelines develop unneeded red tape, leading to even more documents and slower financing handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) rule and the Ability-to-Repay (ATR) demands, while intended at protecting consumers, can bring about delays in closing bargains and enhanced functional prices.

{kind=link}

Table of Contents

Latest Posts

Byob

Using Whole Life Insurance As A Bank

My Own Bank

More

Latest Posts

Byob

Using Whole Life Insurance As A Bank

My Own Bank